To be, or not to be? That is the recession.

Economic outlooks seem to change month-to-month, and yet again, we find ourselves in a unique moment in time. The Fed rapidly switched from loose to contractionary monetary policy in March and recently increased the federal funds rate once again. The effects have yet to curb inflation, which is still at a 40-year high. While prices are rising, the cost to borrow has also gotten more expensive, which is dampening demand. We are starting to see this play out in the housing market. We are noticing more inventory coming to market, coupled with fewer sales. We must, however, provide a caveat: The housing inventory is still historically low. As rates rise, especially as rapidly as they have this year, buyers can get priced out of the market quickly and must reconsider their budgets.

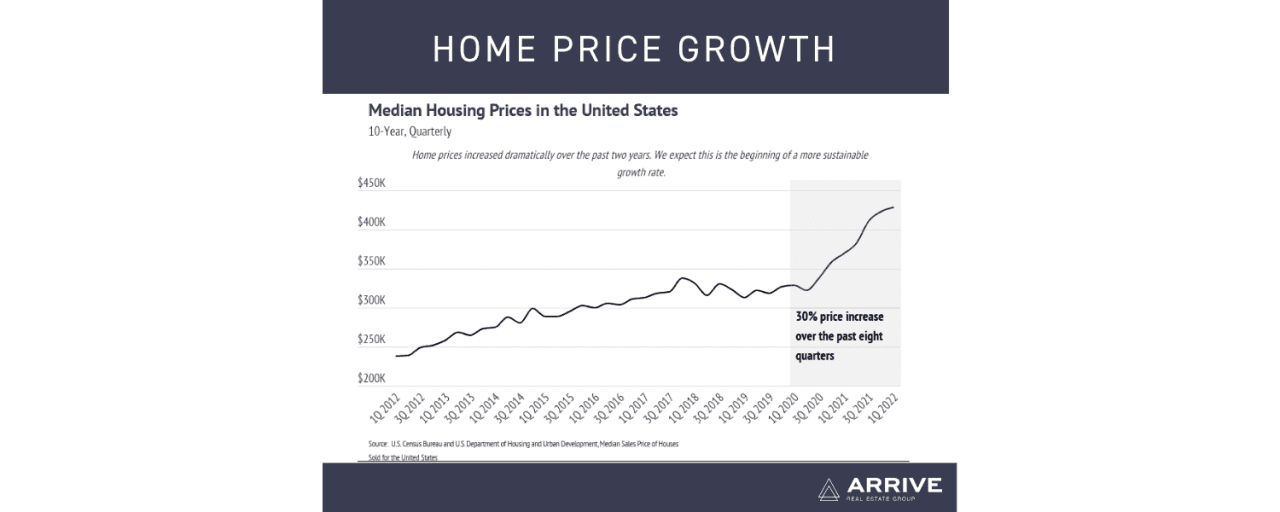

A year ago, the average 30-year mortgage rates hit their lowest levels in history and have more than doubled since then, to 5.81%. In the first half of 2022: The S&P 500 declined 21%, the NASDAQ is down 30%, and Bitcoin and Ethereum have dropped 59% and 71%, respectively. At the same time, U.S. housing prices increased by 15% nationally. Home prices, simply, rarely go down. One lasting effect of the 2006 housing bubble is the perception that home prices decline much like other risk assets, which isn’t the case. Stocks, bonds, and cryptocurrency are fungible assets that allow for large, multiplayer markets. The housing market has only recently become more efficient because of technology, but too many factors play into a home’s value, preventing regular downturns in the market. Large declines in liquid assets do affect demand for homes, though, as people tend to reconsider buying when they feel (and objectively are) less wealthy during dips in those markets.

But what about the Fed’s intention to slow down the economy by decreasing demand through raising rates? Won’t that cause a recession and lower home prices? The Fed’s goal is to slacken growth enough to curb inflation, but not enough to send the U.S. into a recession, which is a challenging needle to thread. The National Bureau of Economic Research, which officially declares recessions, defines a recession as a significant decline in economic activity spread across the economy that lasts more than a few months and is normally visible in real GDP, real income, employment, industrial production, and wholesale-retail sales. With unemployment near all-time lows and a surplus of job openings, we may end up avoiding an official recession, even if GDP decelerates for multiple quarters.

The Local Lowdown

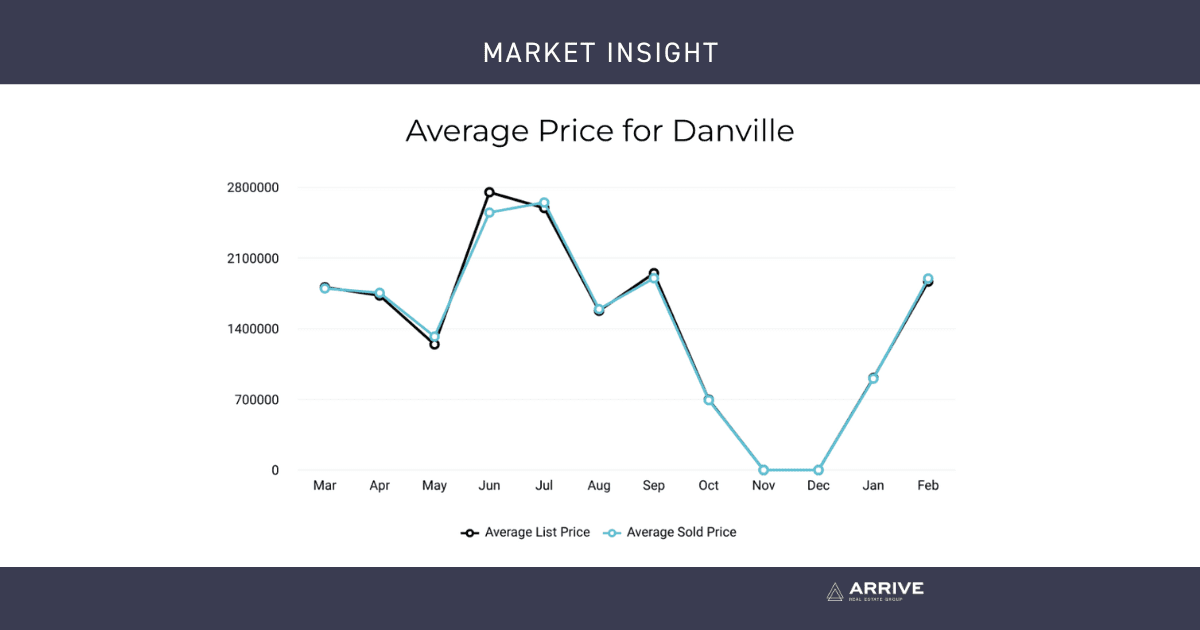

Median single-family home prices in Alameda and Contra Costa declined month-over-month, just below the May peaks, but they’re still historically high. After two years of significant price growth (+38% over the past two years), it’s hard not to think that rate increases have caused prices to creep near a ceiling. Without the aid of super low financing options, fewer potential buyers will participate in the market. So far in 2022, the average 30-year mortgage rate has increased over 2.5%, which equates to an approximately 33% increase in monthly mortgage payments. In other words, the new mortgage rate adds $1,460 per month on a $1,000,000 30-year fixed mortgage. The same price becomes more expensive, unless you are buying with cash.

It’s so incredibly easy to get wrapped up in the recent past, during which home prices grew massively. We can’t stress enough how uncommon that price growth was and, most likely, will continue to be. Because homes are also investments, a steadier growth rate of 6–8% annually is still good for investing purposes.

The East Bay’s housing inventory continued to rise in June, following historical seasonal trends. Since Q4 2019, inventory has trended lower and settled at a depressed level. There were nearly 1,000 fewer single-family homes on the market in June 2022 than in June 2019. Although the first half of 2022 had one of the lowest inventories on record, we were pleased to see that inventory increased, a trend that usually holds until mid-summer. With June inventory continuing to rise, the next two to three months will likely show us peak inventory levels for 2022.

If you were waiting for rates to drop, they most likely won’t. The low but rising supply continues to make the market competitive and, as more homes come to market, could mark the early stages of market normalization. As always, we will continue to monitor the housing and economic markets to best guide you in buying or selling your home. Contact Arrive Real Estate Group today to learn how to make the maximize the equity in your home.